If you want to build a career that you control, you need to learn how to invest in yourself first. Right now there are millions of artisans, entrepreneurs and intrapreneurs taking control of their lives and building their own jobs instead of relying on others to give them a raise or a new opportunity.

We’ve talked to some of them on the Podcast. Have you subscribed?

Investing in yourself is life principle #1 if you want freedom, control and sanity in your work-life.

This gets easier when you start to view every decision you make as an investment - one with an expected cost (in time, money or tradeoff) and an expected payoff (what you’ll get out of the investment).

I argue that investing in yourself carries the highest return on investment for most people. That’s because it leverages most peoples’ largest asset - their lifetime ability to earn money.

If you haven’t thought of this as your largest asset, consider this:

The average lifetime earnings for an American is around $2 million.

What else do you have that is valued at $2 million?!

Viewed from this light, making an investment of $2,000 in a course that could increase your earnings potential by 5% is worth $100,000!

That is a 500% return on investment (ROI), and that return continues to compound as you add and combine skills.

Related: Helping Students and Job Seekers Make Smart Choices About Education, Careers, and Debt

Every Career Decision Is An Investment Decision

There’s a difference between spending and investing. When most frugal people pay for something, they only view it as spending. The key difference is that investments have an expected return on investment.

In this context, I define expected return on investment as something of value you expect to receive that far outweighs the initial spend over a long time horizon.

Will new shoes make you better? Unlikely over the long term - that’s spending.

Will spending money on a course to learn a new skill make you more valuable? You bet - that’s a good investment.

Don’t get me wrong, not all spending is bad, but Investments aren’t just about money. Most career decisions are about investing an even scarcer resource - your time.

On average, people spend over 90,000 hours working over their lives and over 50% of people have unhealthy work-life balances. Allocating your time better is an investment decision that you need get better at each and every day.

If you want more money, more time or more freedom, it’s your responsibility to develop the skills you need to get what you want. No one else can do this for you.

I put together this guide to share how I think about investing in myself to build a better career, and give some actionable ideas for you to build a roadmap of lifelong learning.

How I Learned the Lesson of Investing in Myself

In my early 20’s I was a derivatives trader. It was an extremely high-stress environment, and I watched a lot of older traders struggle with transitioning out of that business.

As the stress got to me, I knew I needed to transition to a new career path, but was so worried about the unknowns of switching in the middle of a recession (this was 2008-2009).

I was locked into this idea that my career had to be a linear journey “up and to the right” (the trajectory if you were looking at my life on a graph).

What I thought success had to look like:

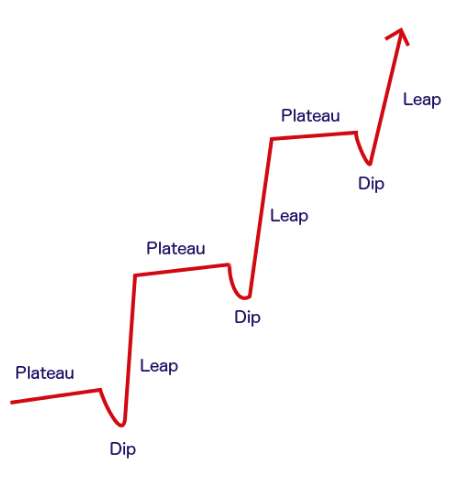

I thought this until I read “The Art of Learning” by Josh Watzkin. There’s a chapter titled “Investment In Loss.” The basic idea of this chapter is that many times we have to take a step backward (loss) to make a giant leap forward. You end up investing time or money to make a tradeoff that will get you on a better path.

What success actually looks like with “investment in loss”

In my case, if I quit, I’d be trading my future earnings for a period of time for a higher level, more valuable and more fulfilling career path.

I could suddenly view the time and money it would take me to move into a completely new career as an investment in my future, and I quit my job the very next day. Here’s a video I did about this period in my life.

This chapter led me to view everything in life as an investment, and recognize that the more I could invest in myself, the better.

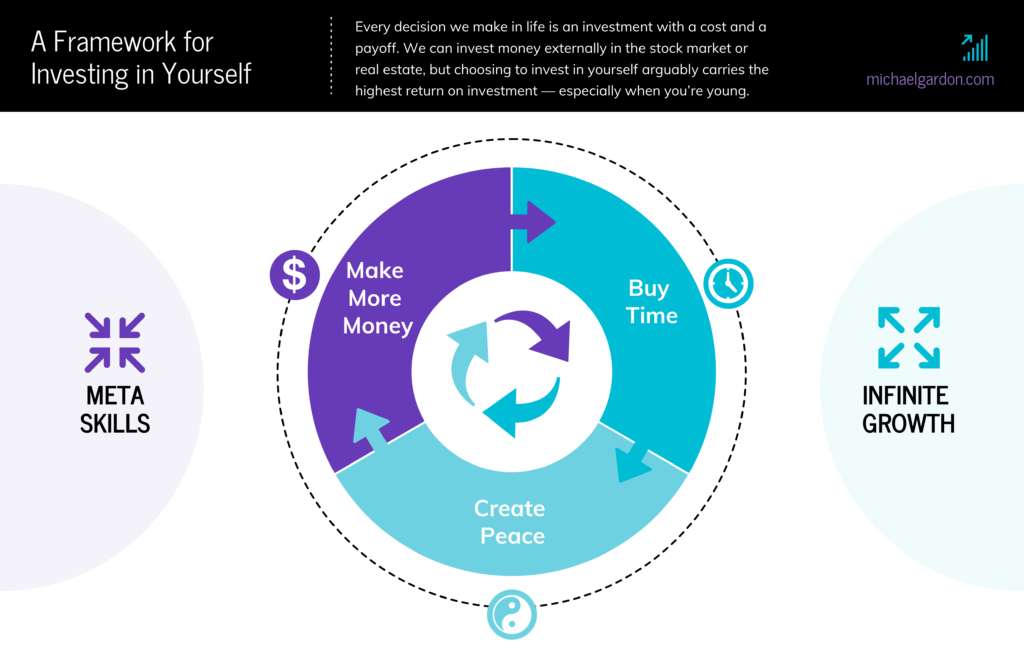

A Framework for Investing in Yourself

I created a framework for investing in myself, which I first wrote about on Goodfinancialcents.com. I’ve adapted it here to apply specifically to career decisions.

From my experience, I’ve come to the conclusion that investing in yourself is done for any of three reasons:

- To create more money (your job)

- To create time (your life)

- To create peace (your work-life)

This is a reflexive cycle that starts with having more money (or at least enough). In the beginning, to make more money you have to trade your time and/or small amounts of money to acquire new skills that make you more valuable in your career, and will lead to more money. Here’s what this framework looks like.

How time, money and peace work together

Your career is a large asset that can be leveraged to work across all three when you view your career as integrated into your life. Tactically, there are high-leverage skills that, when applied to your career, also work across money, time and peace. I call these meta skills.

When we’re just starting out, we usually have time and no money. So, we trade our time for money and gain skills that, guided by experience, make us more valuable. As we gain more money, we start to use that money to buy more time or convenience, which gives us more peace of mind, or time to invest in our health and happiness.

Once you attain a certain level, experts say this is around $75,000, this process also works in reverse. Any wealthy person will tell you that investing in your peace — by cultivating a calm mind, good judgement and healthy body ends up making you more money and creates a better balance with your time.

The kicker is that you can get to peace faster by creating work life balance. This starts with loving what you do.

How to Invest in Your Career in 6 Steps

The best way to invest in yourself is just to start. However, I tend to think in frameworks and steps to sequence my choices to see if I’m on the right path or if I need to course-correct. These steps have been helpful to me in my self-investment journey.

1. Internalize the Difference Between Spending and Investing

Learning this difference is key to your mental framing and attitude toward using money to better yourself and your quality of life.

It’s very hard to incorporate the future into our decisions today, so a ton of our attitude around spending comes from a place of scarcity - I have dollars today, and if I’m going to spend I need to understand what I’m getting and see benefit immediately. It’s very difficult to spend money today in anticipation of some benefit later on, but this is the very definition of investing.

When we spend money we’re usually trading it for a very short term payoff that doesn’t usually on perishable goods that we might need for survival, OR on anti-necessities that have a very fleeting payoff. Think: candy, cigarettes, bedazzled iPhone cases, new cars, etc.

When we invest money, we are expecting a durable, long-term payoff in one of the three areas of the framework above. Think: learning a skill, freeing up time to spend with family, getting in shape, etc.

Join The Break Community

We tell ourselves a lot of stories about money. When I was young, I felt that money was a scarce resource that had to be hoarded. So, I just added money to a pile like Scrooge McDuck, and didn’t use money at all. As I’ve learned more, and had kids that have given me perspective, I’ve come to this conclusion:

“Money is only a tool, which can be leveraged to help you live the life of your choosing.”

Money is only valuable if used productively — and you get to define “productive” use. When I made this subtle mental switch, I got better with using money to improve my life instead of keeping it so my ego could watch my bank account go up. Now, every use of money’s an investment to either increase my wealth, increase my time or increase peace in my life.

Action step:

Make a quick list of the top 10 things you spend money on and the top 10 things you are thinking about spending money on.

For each, note the following:

- Is the payoff likely to last a long time, or will it fade quickly?

- Will the spend make you a better person over the long term?

- Will the spend take care of other, smaller problems that are likely to occur over and over again?

If the expenditure improves you as a person, solve problems, and last a long time, you probably have an investment.

2. Understand Your Circle of Competence

Circle of competence is a mental model popularized by Warren Buffett. It means know the edges of your knowledge and capabilities, and be honest with yourself about what you know and don’t know. Then, either stay inside your circle, or seek to expand it smartly.

When we invest in ourselves, we’re, by definition, trying to expand our circle of competence. But if we don’t know the boundary, we don’t know what will expand our circle versus create a different, less-effective circle, that doesn’t leverage the huge body of experience we’ve built over the years.

Defining your circle isn’t formulaic. It’s just a matter of taking stock of your skills, knowledge or abilities, and being brutally honest about what you know and what you don’t yet know — what you think you know and what you’d like to find out.

Action step:

Write down a list of your skills. Ask people for help if you need more ideas. Once you have a list, categorize your skills into common buckets such as “communication”, “programming” or “digital marketing”.

Hang onto this list for the next step.

3. Figure Out Your Highest Point of Leverage

Because what you don’t know is infinitely larger than what you do know (See Ray Dalio’s book Principles), the next step is figuring out what you should learn. Since time’s finite, there are lots of things you should NOT learn. The goal in this step is figuring out what area of your circle of competence gives you the best growth.

For example, everyone wants to learn ‘coding’. I have my kids learning how to code — I think it’s an essential skill for their future. But not essential for mine. No matter how much I learn, I’ll still need to hire someone better than me to do the software development I need done. So, the time investment isn’t a good one for me; it doesn’t leverage my past experience, or ladder-up to some outcome goal in my life.

My highest leverage points are allocating capital and operations (getting people and processes in place). Any investment I can make to become a better decision-maker or run better systems gives me the most growth in money, time or peace.

Action step:

Take your circle of competence from step two, above, and define the circle as narrowly as you possibly can. For example, “my circle of competence is allocating capital and building small teams that build durable long term value.”

By narrowing your circle, you become aware of what you’re truly good at now, AND the number of areas within your circle you could get better at very easily.

So, if I simply defined my circle of competence as digital marketing, but my highest point of leverage is in building teams, I probably shouldn’t learn how to design in adobe photoshop, or learning Java. I’m better off seeking skills that help me lever the teambuilding or operational side of “digital marketing”.

4. Identify the Skills You Need That Give You More Leverage

Now that you’ve identified your highest point of leverage, there are various individual skills to learn that’ll help you level-up and grow. This step is about deciding which skills to develop.

In the last step I said my highest point of leverage was investing. Within investing there are many skills that I could learn: risk management, making better decisions, charting, real estate investing, stock market investing, cryptocurrencies, hedging, etc. So what should I focus on now?

Action step:

Lay out all of the skills you could learn within this area, that are tangential to your highest point of leverage.

5. Create a Time-Bound Roadmap to Acquire These Skills

Based on your time and money budget, lay out a plan to acquire these skills in sequence. Here’s an example of my tracking spreadsheet that I’ve used in the past to learn some new Excel skills:

It doesn’t matter how you organize it, but a tried-and-true lesson of goal setting is carving out time and breaking down your goal into manageable action plans.

Action step:

Take your list from step four, above, and prioritize your roadmap.

6. Ask for Help

If you’re struggling with any of the steps above, it’s important to ask for help. The biggest problem areas for young people tend to be identifying a circle of competence, and deciding which skills to acquire. This is where help from an outside party can really help.

How can you do this?

- Invest some money taking people out for coffee and ask

- Create a google form with specific questions about your skills and abilities. Send it to a bunch of people you know.

- LISTEN for what people say to you about where you’ve helped them, or where they think you’re smart

Through this process, I started to identify my circle of competence. Part of it happened to be asking great questions, summarizing problems and breaking problems down into chunks, which helps in investing.

Now, I even use my spare time to consult with people thinking about a career change. Please, feel free to contact me if you need help.

Action step:

Find a mentor that you trust, or even just sit down with a friend and talk-out the problem.

Dealing with Resistance To Growth

“The impediment to action advances action. What stands in the way becomes the way.”

Marcus Aurelius, “Meditations”

That quote is everything you need to know about dealing with resistance. At a gut level, you know what you need to do, you just don’t KNOW for sure what results you’ll see.

Most resistance is a form of fear that comes from one of three places:

- Money scarcity mindset

- Needing certainty

- Option overload

So what helps? How do you overcome resistance and choose yourself?

Following the Steps to Investing in Yourself section will help. Here’s how.

Resistance #1: Money scarcity mindset

When you view money as scarce, you’ll never spend money on yourself — even when you need it to make a growth leap. Just like there’s good debt and bad debt, there’s good spend and bad spend.

Mentally differentiating between frivolous expense and true investment is key. One heuristic I use to differentiate them is this: if a spend makes me better at X (more productive) it’s an investment. For example, most people don’t use any type of resume writing service because they cost money. But getting the job you want is so key to money and happiness, that spending a couple hundred dollars to have it done to the best of your ability is completely worth it.

The truth is, even if you don’t have any money right now, there are designs you can put in place to free up money and get what you want.

Resistance #2: Needing certainty

You don’t know FOR SURE that the investment will pay off, and that scares people because they could face a loss. This is the Loss Aversion Principle in Behavioral Economics, which is part of Prospect Theory (Kahneman & Tversky, 1979). Loss aversion is the tendency to prefer avoiding losses to acquiring equivalent gains.

To get over this, you have to expect a long-term payoff, but also acknowledge that any single event might not work out, so play the long game.

In life, almost every decision worth making has an uncertain payoff. We have to decide to grow and trust that we’ll produce the result we want over the long run.

The hack I use to get around this problem is what I refer to as “sizing” or “options betting”. In investing, sizing refers to making your position big enough or small enough so that you get comfortable with a given risk. This always works. Same with investing in yourself. If a $2,000 course is too much money, how can you learn some of the concepts with YouTube and four hours of your time?

What I call “options betting” refers to dealing with uncertain outcomes by creating a few options for how to tackle a problem, thereby increasing the chances that one approach works. Then, betting heavier when you’re more certain about the right approach. You can try this for yourself by testing three different ways to learn a skill to see which way you learn better.

Resistance #3: Option overload when starting

While we need to use options to get over uncertainty, having too many options is a killer for focus.

This is the hardest to overcome because these days we can literally learn anything, and a superpower is focusing on what’s the best use of our time.

Your filters for excluding options have to be Circle of Competence and Highest Point of Leverage as discussed above. If this doesn’t make sense, go re-read those sections or ask me a question.

Your circle of competence tells you what you’re already knowledgeable about and have some skill in (to build from). Within your circle of competence is your highest point of leverage — the one or two unique talents you have, that when applied, supercharge your effectiveness, creative energy, production, etc.

When you’re really clear about these two aspects, you’ve weeded out 95% of options that might get in the way of your decision, and now you’re free to focus on a handful of skills that’ll likely have the highest return on time and money for yourself.

Related: The Eisenhower Matrix: Your Simple Decision-Making Tool to Get More Done

Bringing Career Investment Home

Deciding to invest in yourself to improve your career situation is the #1 decision that separates people who become fulfilled, and those who continue to struggle at their job year after year. I learned this lesson the hard way, and I hope that these words help you avoid some of the pain I’ve gone through trying to find and build out my circle of competence.

If you want to hear more on this topic, check out michaelgardon.com or drop me a note in the comments.

Grab a PDF of this article!

Do you want to save this article to reference later? We compiled this article so that you can reference it later!